Buying vs. Renting a Home: Short-Term and Long-Term Benefits

Nima Kazeroonian November 10, 2025

Nima Kazeroonian November 10, 2025

Buying vs Renting

Deciding whether to buy or rent a home is a personal choice that depends on your financial readiness, lifestyle and timeframe. In high-cost markets like the Bay Area, rent can be comparable to mortgage payments but rents often increase at faster rates while a fixed-rate mortgage remains stable. In the short term, renting is attractive because the upfront costs are low, you don’t need a large down payment, and you have flexibility to move for jobs or lifestyle changes. Renting also means you can call your landlord for repairs and avoid maintenance headaches. However, each rent check goes toward someone else’s investment, and you may face unexpected rent hikes down the line.

Buying a home has a higher upfront cost—down payment, closing costs and maintenance—but offers long-term benefits. From day one, part of your monthly payment builds equity in an asset that could appreciate over time. Mortgage interest payments may be deductible and homeowners can deduct a portion of state and local taxes. A fixed-rate mortgage also provides payment stability, shielding you from the rent increases that many tenants experience. Over a longer horizon, homeowners have the opportunity to leverage their property for loans or enjoy substantial gains if the market appreciates.

Short-term, renting might make more sense if you anticipate moving within a few years or need time to build savings and credit. The flexibility of a lease allows you to change neighborhoods or downsize without the transaction costs of buying and selling a property. If you have a clear long-term plan and are financially ready, buying can be a strategic move to build wealth. Even though home prices and interest rates have risen, monthly mortgage payments in many markets are close to rents, and the stability of ownership can be worthwhile.

Long-term, owning a home generally becomes more cost-effective. Equity accumulates as you pay down your mortgage and as property values appreciate. Over decades, this can provide a significant nest egg or serve as a hedge against inflation. Homeowners also enjoy the freedom to remodel, expand or personalize their space without asking a landlord, which can enhance quality of life. Meanwhile, long-term renters may need to set aside more savings for retirement to account for lifelong housing costs. According to one study, renters face ongoing housing expenses into retirement, while homeowners eventually pay off their mortgages and reduce monthly expenses.

In the end, there is no one‑size‑fits‑all answer. Your decision should align with your financial situation, lifestyle goals and how long you expect to stay in one place. If you’re unsure which path is best, consider working with a real estate professional who can analyze your local market and help you run the numbers. Whether you decide to rent or buy, being informed about the trade‑offs will help you make the right choice for your short‑term comfort and long‑term prosperity.

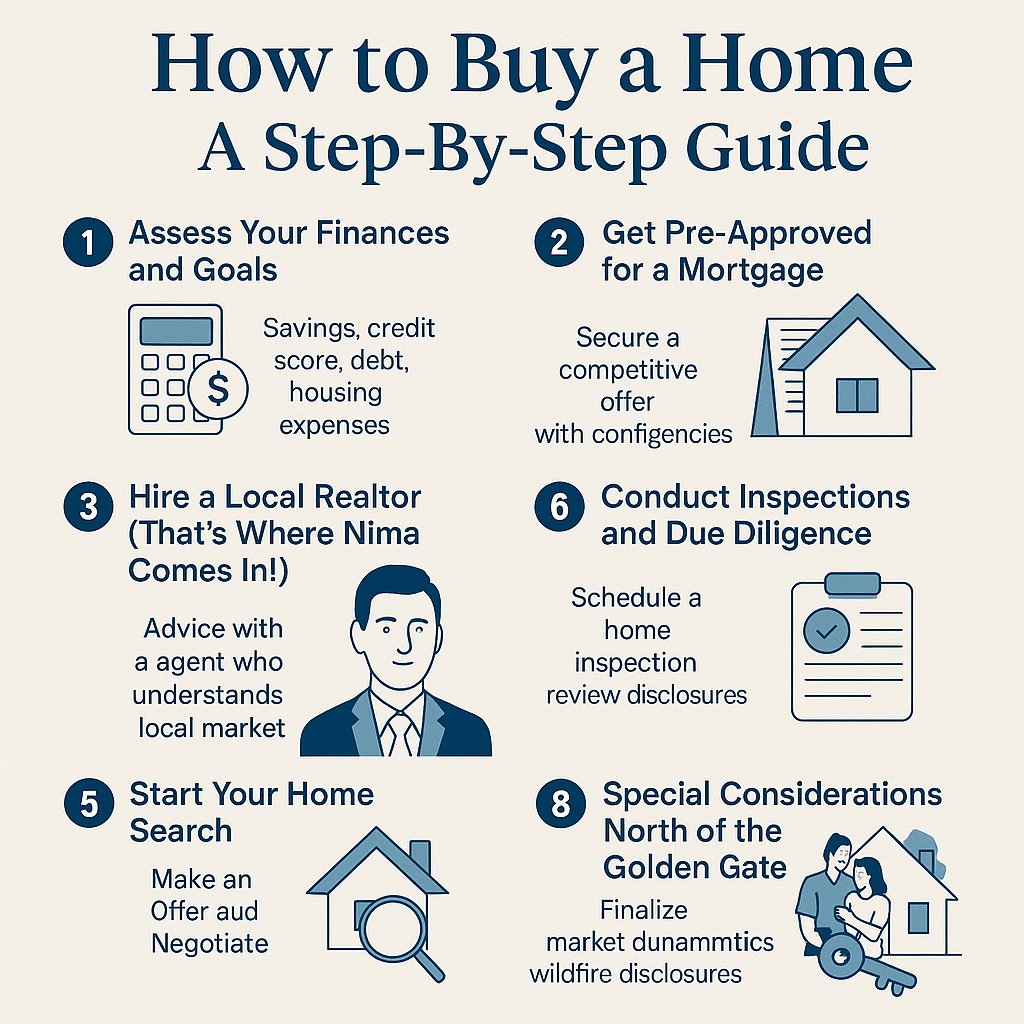

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!