Historical Mortgage Rates vs Today: What Sonoma County Buyers Should Know in 2026

Nima Kazeroonian June 1, 2026

Nima Kazeroonian June 1, 2026

If you’re buying in Sonoma County in 2026, it probably feels like you’re trying to hit a moving target. Rates move, inventory shifts, and every conversation seems to come back to one question: “Should I buy now, or wait for rates to drop?”

Here’s the truth—rates always move. Sometimes slowly, sometimes fast. And for most buyers, the winning move is understanding how rates historically behave, what “normal” really means, and how to structure a smarter offer so you’re protected whether rates rise or fall.

This post breaks it down in plain English: what rates used to be, what today’s rates mean for you, and the strategies Sonoma County buyers should prioritize in 2026.

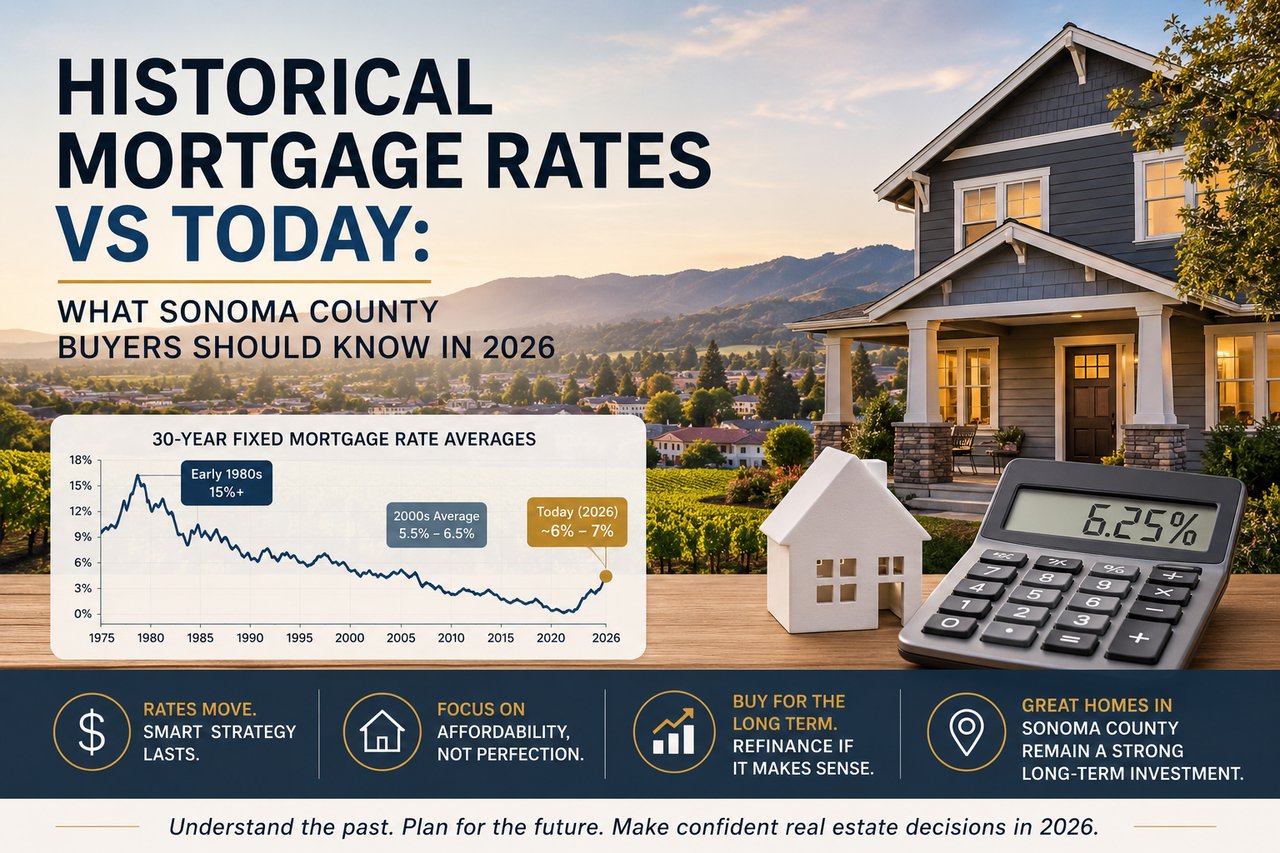

A lot of buyers think “today’s rates are high.” That’s only partly true.

Historically, rates have lived all over the map:

The important concept is this: those ultra-low rates were the exception, not the baseline.

So if you wait for rates to “go back to what they were,” you might end up waiting for a season that doesn’t return in the same way—or you might miss home price appreciation while you wait.

Home prices get all the attention, but rates are the real “budget breaker.”

Here’s a simple way to think about it:

Even a small change in rates can meaningfully shift affordability. For example, the difference between a 6% rate and a 7% rate on a typical mortgage amount can be a few hundred dollars per month—enough to push a home from “yes” to “no” in a lender’s eyes or in your own household budgeting.

For a lot of buyers, this leads to the common delay strategy: “Let’s wait until rates drop.”

That can work, but there are two real risks:

So instead of trying to “outsmart” rates, your best move is to stress test your plan and build a strategy that works across different scenarios.

You can’t control rates—but you can control how you structure your purchase.

Here are the top levers that make the biggest difference:

A simple pre-qualification is not the same as an underwriting-level approval. A stronger approval gives you confidence and helps you act quickly on the right property. Sellers and listing agents can tell when you’re prepared.

Don’t just ask “What can I afford?” Ask:

“What payment range keeps my life stable?”

Then work backwards. Your comfort band is your North Star.

In some Sonoma County deals, buyer-side strategies can lower your payment meaningfully:

These aren’t “magic,” but when used properly, they can turn a marginal payment into a manageable one.

Rates don’t rise or fall based on how badly you want to buy. They move based on broader economic factors. So the better framework is:

A smart mindset is:

Buy for the lifestyle and long-term value; refinance if it improves your life.

Not the other way around.

Sonoma County is highly competitive when demand runs hot. If rates drop meaningfully, you will likely see:

That’s why some buyers decide to buy during “in-between” moments—when rates feel “meh,” but competition hasn’t fully heated up.

Your job is to know your numbers well enough to avoid bidding from fear.

Here’s a practical mental model I recommend:

Every $100,000 borrowed becomes a meaningful monthly payment, and rate changes amplify that reality.

So if your budget feels tight at today’s rate, there are only a handful of ways to fix it:

That’s it. Everything else is noise.

A: Waiting can work, but it’s a gamble. If rates drop, demand and competition often jump—which can push prices up and make winning harder. If you can comfortably afford a home today, buying now and refinancing later (if rates improve) can be a practical strategy.

A: For most buyers, the rate matters more because it drives the monthly payment and affects approval. Price matters long-term, but your payment determines whether you can actually live with the home financially.

A: If you lock your rate before closing, your payment is fixed (assuming a fixed-rate loan). The risk is not that your payment rises—it’s that future buyers might pay less if rates push affordability down. That’s why buying for long-term value and location still matters.

A: They can be, but you need to understand the structure and plan for the payment to rise later. Buydowns should be paired with a realistic refinance plan or a clear comfort level at the higher payment.

The biggest mistake I see in strong markets is the “perfect moment” mindset. Buyers wait for the perfect rate, perfect price, perfect inventory, perfect timing—and the market never lines up that cleanly.

In Sonoma County, the better mindset is:

Because 10 years from now, you’re not going to remember whether your first rate was “good.” You’re going to remember whether you bought the right home in the right neighborhood, with a payment that didn’t keep you up at night.

If you want, tell me your target purchase price range and approximate down payment, and I’ll help you outline (1) what payment to expect across a couple rate scenarios and (2) negotiation strategies that fit Sonoma County deals in 2026.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!