Is the Proposed 50-Year Mortgage a Game-Changer for Homebuyers?

November 12, 2025

November 12, 2025

The concept of a 50 year mortgage has burst onto the scene in late 2025 as policymakers search for ways to ease the housing affordability crisis. Federal Housing Finance Agency director Bill Pulte and former president Donald Trump have floated the idea of allowing borrowers to stretch their loan repayments over five decades (White House’s 50-year mortgage proposal has one notable benefit but a number of drawbacks). This idea is still only a proposal; current federal law caps government backed mortgages at 30 years. Because the product does not yet exist, it’s premature to call it a “good” or “bad” innovation. Instead, it’s helpful to examine the potential benefits and risks for different types of buyers.

The primary appeal of a 50 year loan is obvious: spreading principal and interest over a longer term reduces the monthly payment. Analysts estimate that on a median priced U.S. home, monthly payments could drop from roughly $2,288 to around $2,022 if the interest rate is the same as a 30 year loan (White House’s 50-year mortgage proposal has one notable …). In another example, a $500,000 home financed at around 6.2 % might see the payment fall by about $280 compared with a 30 year mortgage (What a 50-Year Mortgage Would Mean for Home Buyers). Even though the savings aren’t huge, that extra $200–$300 a month can make a difference for budget constrained buyers in high cost markets.

Lower monthly obligations could allow some aspiring homeowners — particularly younger buyers and those without significant savings — to qualify for a mortgage they otherwise couldn’t afford. For investors or people with multiple properties, a longer amortization could free up cash flow for other investments or home improvements. Some advocates see the product as a way to provide an “entry point” for first time buyers who are currently stuck renting (What a 50-Year Mortgage Would Mean for Home Buyers).

Extending a mortgage term to 50 years dramatically increases the total interest paid over the life of the loan. One analysis found that a borrower might pay roughly $389,000 more in interest on a median priced home compared with a 30 year loan (White House’s 50-year mortgage proposal has one notable …). Because the payments are stretched over five decades, much of the early payment goes toward interest rather than principal, slowing the pace of equity accumulation. In fact, homeowners with 50 year loans could still owe hundreds of thousands of dollars when borrowers with 30 year loans own their homes outright. That lack of equity also makes borrowers more vulnerable if home prices fall, potentially leaving them underwater.

Another concern is that lenders would likely charge a higher interest rate to compensate for the increased risk of a longer term. If the rate is even a half point higher than a comparable 30 year mortgage, most of the monthly payment savings could disappear. Critics also note that a 50 year mortgage doesn’t solve the underlying problem of limited housing supply and may even drive up home prices by increasing buyers’ purchasing power (White House’s 50-year mortgage proposal has one notable …). Perhaps most important, a 50 year loan could keep borrowers in debt well into their retirement years; a 30 year‟old borrower could still be making mortgage payments at age 80 (What a 50-Year Mortgage Would Mean for Home Buyers). That may complicate retirement planning and intergenerational wealth transfer.

Because the product is hypothetical, it’s impossible to know exactly how lenders would structure a 50 year loan or who would qualify. However, certain types of buyers might find it useful.

The 50 year mortgage is still just an idea. Its benefits — smaller monthly payments and easier qualification — are tangible but relatively modest. The trade‟offs, including slower equity growth, significantly higher total costs, possible higher rates and potential for extended debt into old age, are substantial. Housing experts caution that the proposal does nothing to increase the supply of homes and may even raise prices. Because the concept is so new, labelling it a bad idea or a silver‑bullet solution would be premature. Prospective borrowers should watch how policymakers and lenders flesh out the details and consult with trusted real estate and financial professionals before deciding whether such a loan fits their circumstances.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

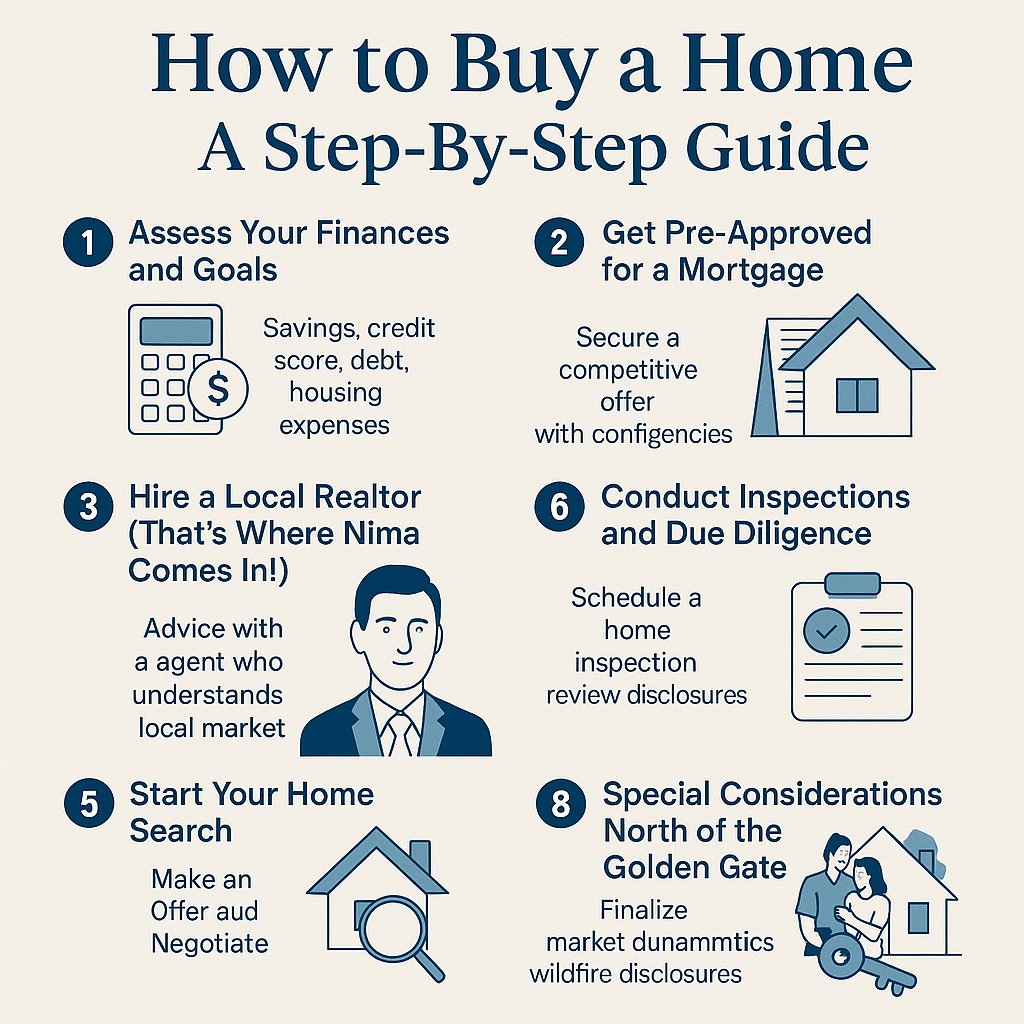

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!