Mortgage Rates Are Rising Again in 2026: What It Means for Sonoma County Home Prices

Nima Kazeroonian March 24, 2026

Nima Kazeroonian March 24, 2026

Mortgage rates are climbing again, and it’s happening at a moment when Sonoma County buyers and sellers are already recalibrating their expectations. After dipping below 6% earlier this year, the average 30-year fixed rate has been moving higher; Freddie Mac reported it averaged 6.22% as of March 19, 2026, up from 6.11% the week before. Rates aren’t back at their 2022–2023 highs, but they’re high enough to meaningfully change monthly payments—and that changes buyer behavior fast.

The big question everyone asks is simple: “Do rising mortgage rates make Sonoma County home prices go down?” The honest answer is: rising rates often create downward pressure, but they don’t guarantee falling prices—because home prices are also strongly influenced by inventory, local demand, and how many sellers are actually willing (or able) to list.

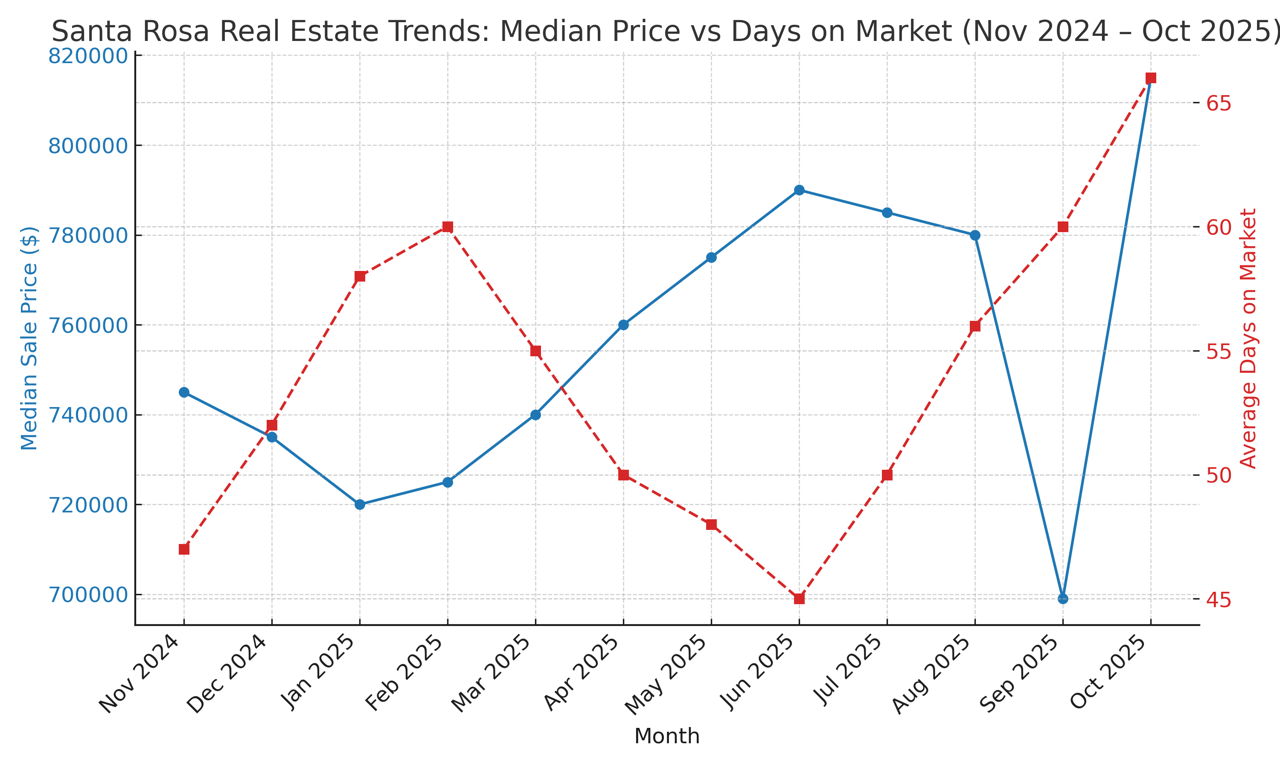

In Sonoma County, the story isn’t as dramatic as headlines sometimes suggest. Even with affordability tightening, the market remains active—just more cautious. According to Redfin, Sonoma County home prices in February 2026 were down about 5.3% compared to a year ago, with a median sale price around $782K, and homes taking longer to sell on average than they did last year. That doesn’t mean a crash; it usually means buyers are negotiating harder, sellers are adjusting pricing strategy, and “too high” homes simply sit.

Let’s break down what this new rate environment means for both sides—and what you can do about it.

Mortgage rates move with bigger economic forces: inflation expectations, the bond market (especially the 10-year Treasury yield), and global instability. In early 2026, rates moved higher amid renewed inflation concerns tied to geopolitical tensions, pushing Treasury yields up and dragging mortgage rates along. Even if the Federal Reserve isn’t actively hiking rates week-to-week, the market still reacts quickly to uncertainty.

For Sonoma County, this matters because our price point is already high relative to many parts of the U.S. That means even modest rate moves translate into big payment changes. On a typical Sonoma County price level, a small rate bump can remove a chunk of the buyer pool—not because buyers disappeared overnight, but because qualification limits and comfort levels get hit.

One of the most important realities of rising rates is this: affordability changes instantly, but prices change slowly.

If a buyer was shopping at 5.5% and now sees 6.2%+, the monthly payment jumps significantly for the same home price. To illustrate, imagine a purchase around $782,000 (roughly in line with recent local median sale price levels). With 20% down, financed over 30 years:

That’s not a slight inconvenience—that’s the difference between feeling confident and feeling stretched. When buyers feel stretched, they either lower their search price, ask for concessions, or pause entirely.

This is why “softening” can show up first as:

…and only later as broader price declines.

If you’re a buyer, rising rates feel like a punch in the stomach—but they can also create an opportunity if you approach the market strategically.

Here’s what I’m seeing (and what tends to happen historically):

The key for buyers: don’t try to time the bottom perfectly. Focus on buying a home you can afford comfortably, with a plan to refinance later if rates drop.

For sellers, rising rates don’t necessarily mean your home value is collapsing—but they do mean your margin for error is smaller.

Here’s what typically changes in a rising-rate environment:

If you’re thinking of selling in 2026, your best move is to focus on three things:

No amount of optimism will overcome a mispriced listing in a market where buyers feel payment pressure every day.

So, will home prices fall?

They might soften—or they might flatten—depending on inventory. If more sellers list because they feel “this is the moment,” and buyers retreat because payments are high, prices could slip. But if inventory stays tight (the Bay Area is famous for it), prices can stay surprisingly resilient even with higher rates.

A useful signpost: Zillow’s Sonoma County overview shows the average home value around $782,003, down about 2.5% year-over-year as of late February 2026. That’s a gentle slide—not a crash—consistent with what you’d expect when demand is cooling but supply hasn’t exploded.

Whether you’re buying or selling, rising mortgage rates are basically telling everyone the same thing:

Get serious about strategy.

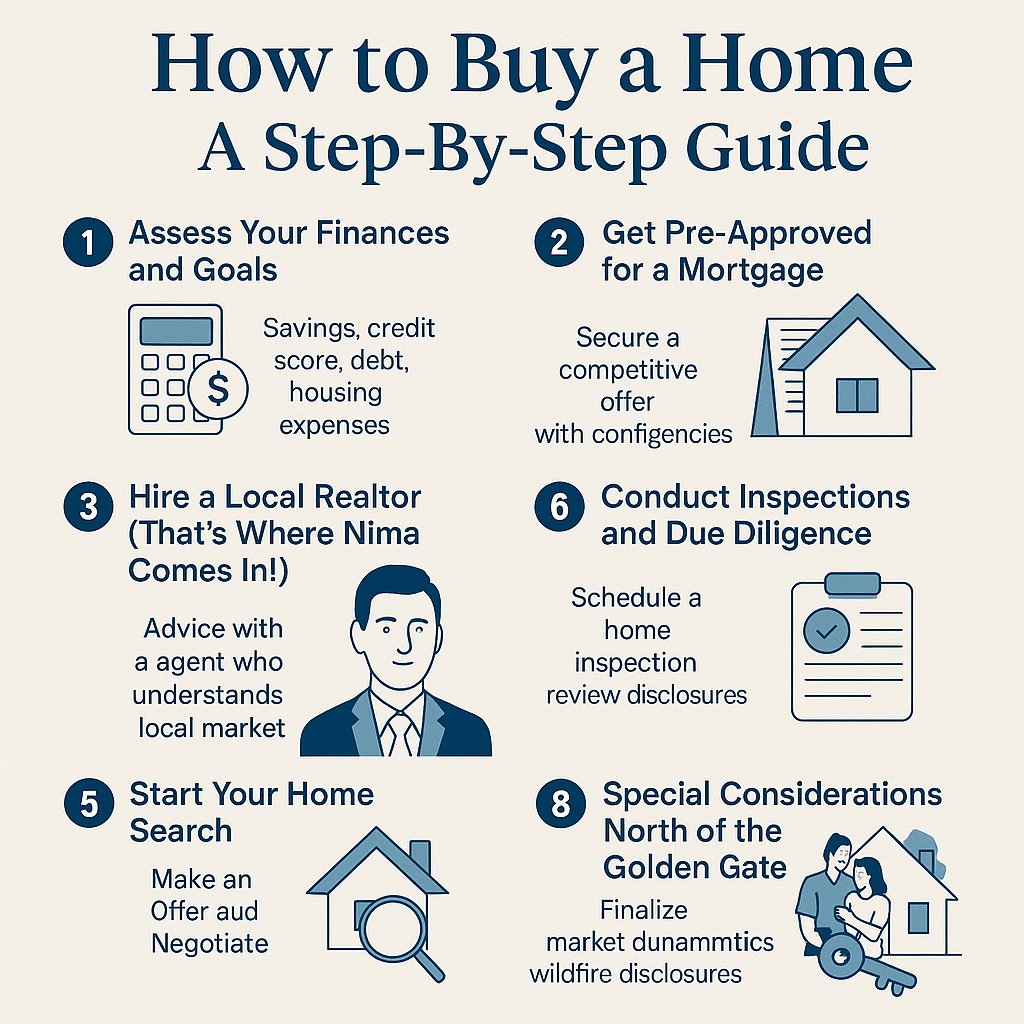

If you’re unsure how rising rates specifically impact your plan, let’s talk. The “right” answer depends on your timeline, your home’s condition and location, and what you’re trying to achieve this year.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!