Should You Sell Your Sonoma County Home Before Mortgage Rates Drop Again?

Nima March 10, 2026

Nima March 10, 2026

Should You Sell Your Sonoma County Home Before Mortgage Rates Drop Again?

There’s a common myth that the “smart” move is to wait—wait for mortgage rates to drop, wait for buyers to become more motivated, wait for a better year.

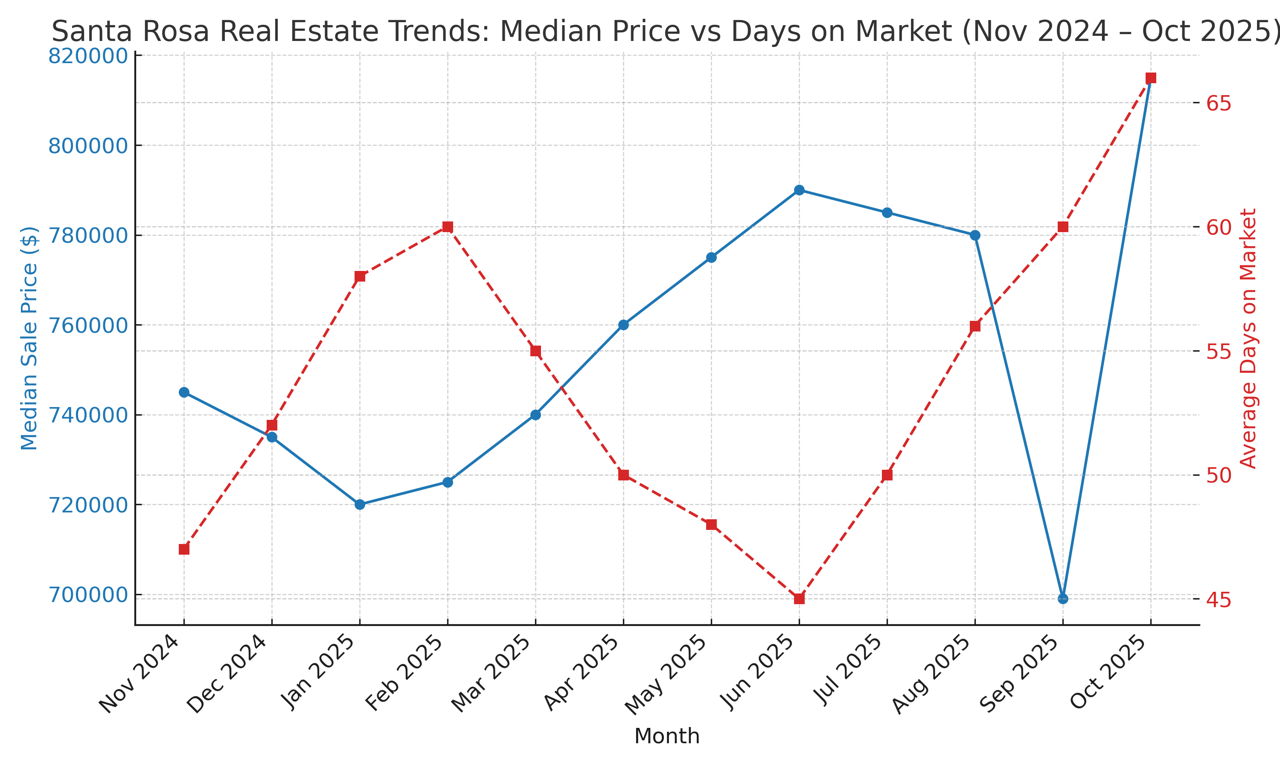

In reality, most homeowners don’t win by waiting. They win by planning. In Sonoma County, the decision to sell isn’t just about rates. It’s about how supply and demand will shift when rates move, what that does to your negotiating power, and how your next purchase fits into the equation.

When mortgage rates fall, the pool of buyers typically expands. That sounds great… until you remember the other side of the market.

If rates drop meaningfully, more homeowners feel comfortable selling. That can bring more inventory onto the market—suddenly, you’re competing with more listings that might offer upgrades, larger yards, and fresh renovations.

The same thing that creates demand also tends to create competition.

And competition is what erodes premiums. So if you sell before the next meaningful rate drop, you may face fewer competing listings, and your home’s uniqueness carries more weight.

Across the country, a huge number of homeowners refinanced into very low rates over the past decade. Many people hesitate to list because they don’t want to give up that payment. That hesitation creates a window for sellers who are ready now.

If you list while most homeowners are still locked in, you’re selling into a constrained inventory environment. If you wait until rates drop enough that more homeowners feel comfortable selling, your home becomes one option among many.

Here’s the big question sellers ask: Will my price be higher if I wait?

Maybe. Maybe not.

If rates drop, it’s possible prices will rise because demand grows. But it’s equally possible that prices rise only modestly while days-on-market increases because buyers suddenly have more homes to choose from. And even if prices do climb, that doesn’t mean your net improves—because you will likely be buying your next home in that same rising market.

So instead of asking, “Where will prices be?”, a smarter question is: Where will my total move-up or downsize cost be?

If you’re planning to buy after you sell, waiting can get expensive. Here’s why:

In other words, waiting often doesn’t help move-up buyers—it hurts them.

Yes, rates matter, and they influence buyer behavior. But your decision should be weighted more heavily toward:

If you’re ready, waiting “for rates” can become an expensive delay.

As of early March 2026, the national average 30-year fixed mortgage rate is around 6.00% (Mortgage Rates) —much lower than the peaks we saw, but still far from the ultra-cheap pandemic era.

Some forecasts expect rates to drift lower over time. For example, one Fannie Mae outlook forecasted rates ending 2026 just under 6% (Mortgage Rates Expected to Move Below 6 Percent by End …). If that happens, demand may heat up—but so may listing activity.

The takeaway: you don’t need to perfectly time the rate cycle. You need to get ahead of the competition.

When I consult with sellers, we look at three practical timelines:

90 days: If your home is already in good shape (or can be quickly refreshed), you can often list quickly and capture demand while inventory is still manageable. This is the best option when you’ve already identified your next move.

6 months: Perfect for homeowners who want to maximize net proceeds without chaos. We make a punch-list of repairs, coordinate staging and photography, and build a launch strategy that aligns with your ideal move date.

12 months+: If you’re a year away, you have leverage. You can upgrade systems, improve curb appeal, and lock in strong presentation. The risk is “market drift”—conditions change—so we still put milestone checkpoints on the calendar.

Here’s a smart, “no drama” playbook:

Will buyers still buy with rates around 6%? Most do. If the home fits their lifestyle and budget, they focus on payment and future refinancing options rather than waiting indefinitely.

Does selling mean I have to buy right away? Not always. Many homeowners use rent-backs, short-term rentals, or a staged move to keep control of timing while they shop for their next place.

Should I list off-market first? It depends, but in many cases sellers maximize value by exposing their home to more buyers—because competition creates better offers.

Selling before mortgage rates drop can make sense if your goal is to capture strong demand with less listing competition and move with more control.

If you wait for rates to fall, you may benefit from a larger buyer pool—but you may also lose the “scarcity effect” that helps sellers win.

If you want a clear, local strategy for selling in Santa Rosa or anywhere in Sonoma County—and a plan that connects your sale to your next purchase—reach out. I’ll give you a customized timing breakdown based on your home, your equity, your timeline, and your next move.

When you’re ready to make this move, you’ll know exactly why—and exactly how.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!