Step-by-Step Guide to the Mortgage Loan Process for First-Time Homebuyers

November 17, 2025

November 17, 2025

Buying your first home is exciting, but the loan process can feel overwhelming. Here’s a breakdown of each phase so you know what to expect from start to finish.

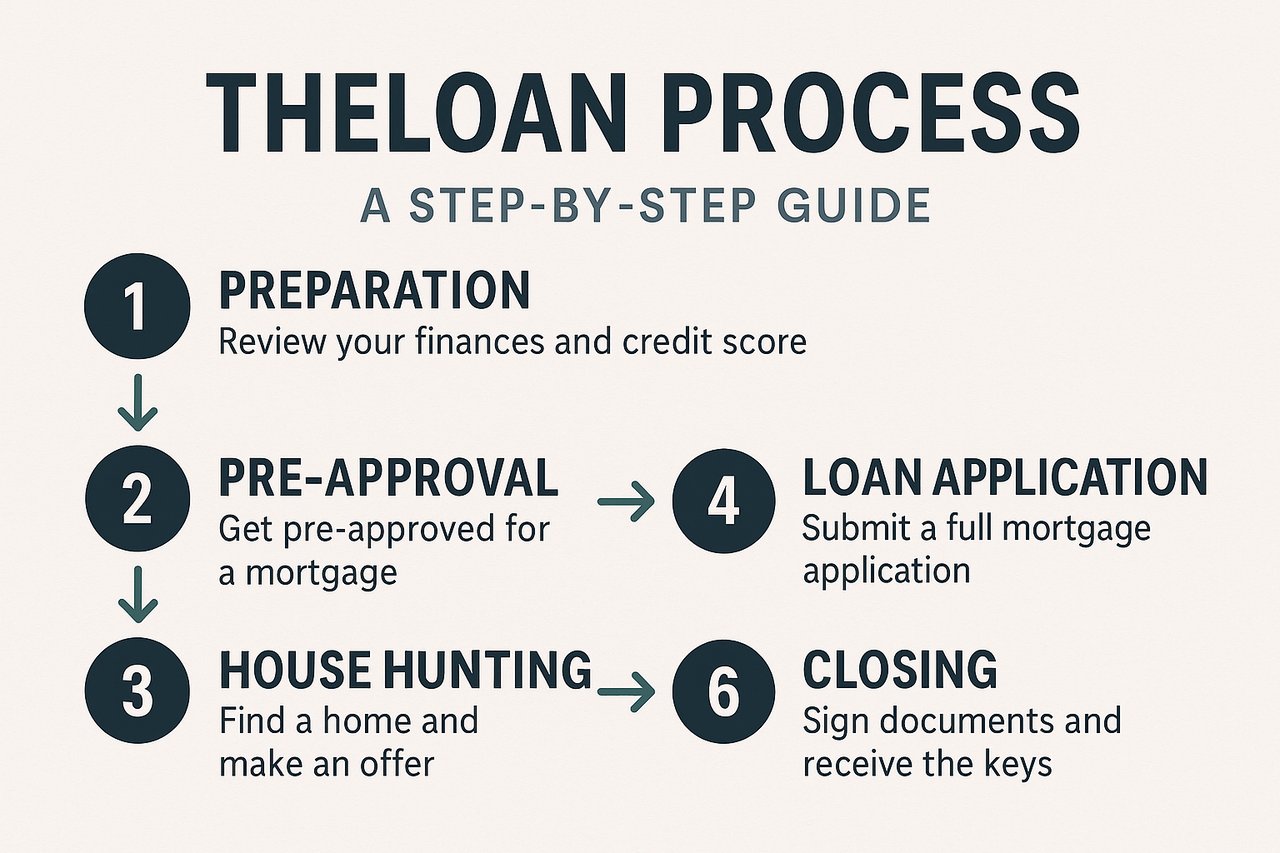

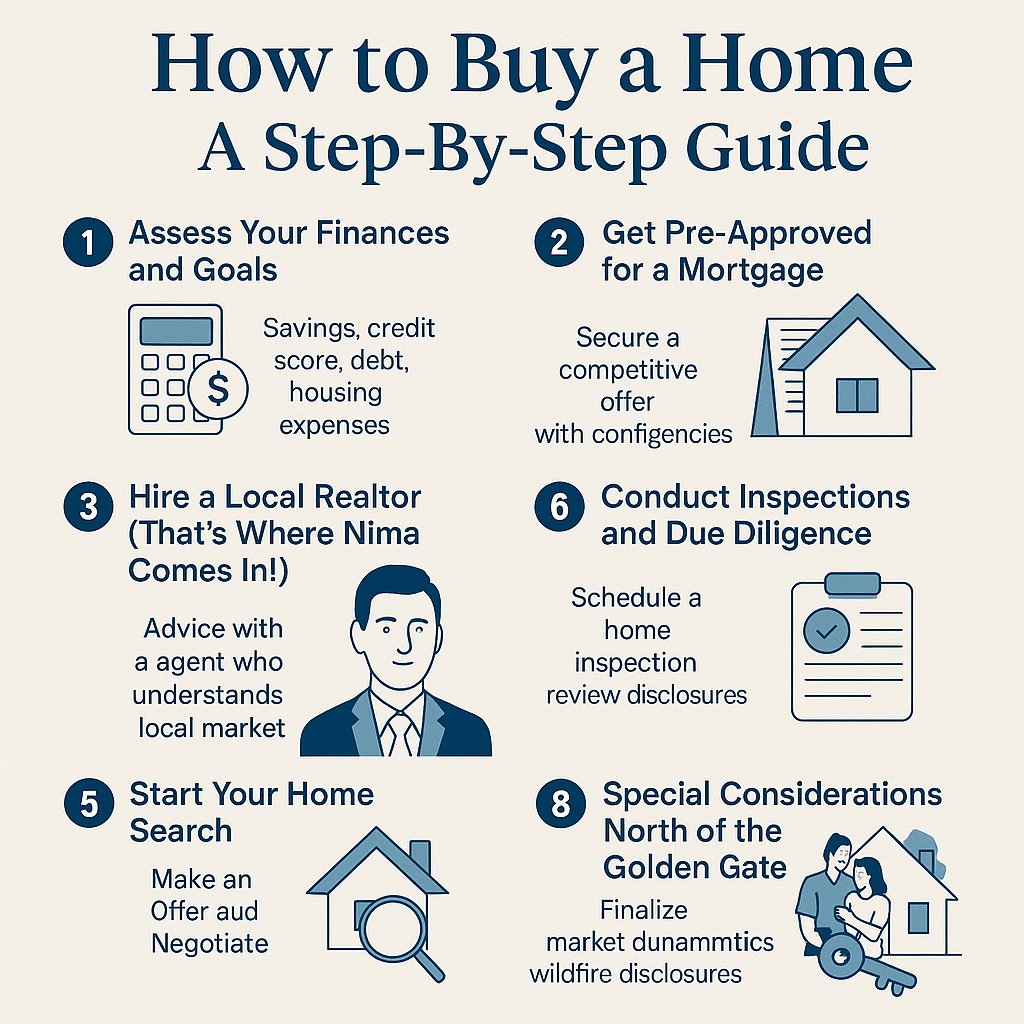

Before you fall in love with a home, review your finances. Check your credit report and score; lenders look at your credit history, income, debts and assets to decide whether to approve a loan. Improve your credit score if needed by paying down debt and making on-time payments. Gather documents like pay stubs, W-2s, bank statements and tax returns.

Next, get pre-approved. During pre-approval a lender analyzes your financial information and tells you how much you may borrow. This step gives you a realistic budget and shows sellers you’re a serious buyer.

With a pre-approval letter in hand, start shopping for a home within your budget. When you find one, make an offer. Once the seller accepts, the formal loan process begins.

You’ll complete a full mortgage application and submit documentation of your income, debts and assets. This is when the lender orders a credit check. Being responsive to your lender and providing requested documents promptly helps keep the process moving.

Schedule a professional home inspection soon after your offer is accepted. This step allows you to identify any issues and negotiate repairs. The lender will also order an appraisal to verify the property’s value matches the purchase price.

Once your application and documentation are complete, your file goes to processing. The processor reviews the documentation and may request additional items. Then it moves to underwriting. The underwriter evaluates your creditworthiness and loan risk by looking at your credit history, debt-to-income ratio, employment status, assets and the appraisal. Underwriters use the “5 Cs” of credit — character, capital, capacity, collateral and conditions — to decide whether to approve your loan. Underwriting typically takes 40–50 days. Respond quickly to any requests for additional information, such as explanations of large deposits or letters of explanation for credit events.

If the underwriter approves your application, you’ll receive a conditional approval that outlines any final conditions to satisfy, such as providing updated bank statements or paying off a credit card.

Once all conditions are met, your loan receives final approval. A few days before closing, you’ll receive a Closing Disclosure that details your loan terms and how funds will be disbursed. Review it carefully and ask questions if anything is unclear. On closing day you’ll sign the final paperwork, pay your closing costs and down payment, and receive the keys to your new home. Multiple parties may attend closing, including you, the seller, real estate agents, the closing agent and possibly an attorney. After funding, the loan is complete and you can move into your new home.

This article aims to give first-time buyers clarity about each step in the mortgage loan process so they can approach their purchase with confidence.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!