The $100K Mistake Sonoma County Homeowners Are Making Right Now (2026 Update)

Nima Kazeroonian March 18, 2026

Nima Kazeroonian March 18, 2026

If you’re a homeowner in Sonoma County thinking about selling in 2026, the biggest threat to your bottom line isn’t the economy, the election cycle, or even interest rates by themselves.

The most expensive mistake is more basic—and more common—than people realize:

Waiting too long to list or pricing like it’s 2021–2022.

That’s it.

On paper, it sounds harmless: “We’ll wait until rates drop and buyers come back.” But in practice, the “wait” strategy often morphs into a slow leak—months of carrying costs, deferred maintenance, rising competition, and price adjustments that look small… until they aren’t.

A six-figure hit doesn’t require some dramatic “crash.” It can happen in totally normal, reasonable market conditions.

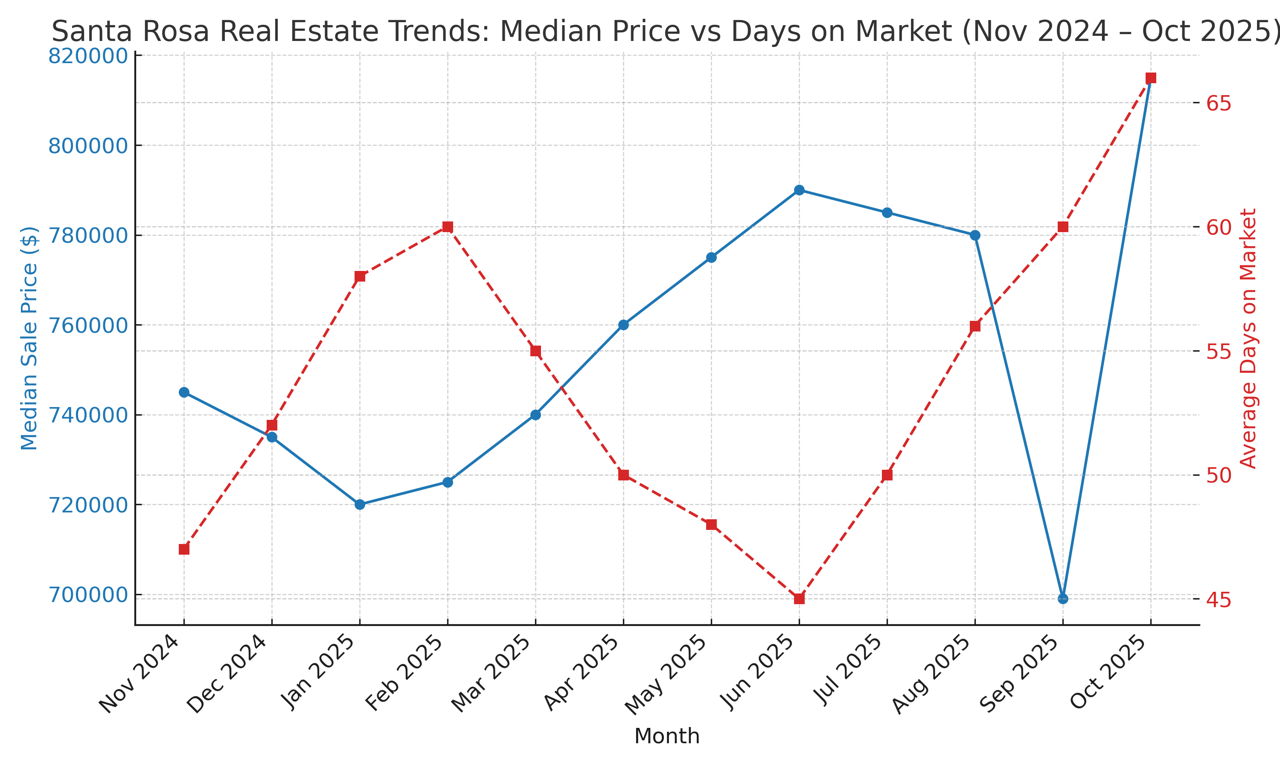

The 2026 housing market is defined by a mix of volatility and “meh.” Mortgage rates have bounced around the 6% range, with some recent reporting showing the 30-year fixed around the mid-6s. That’s lower than the pandemic-era lows buyers loved, but it’s still high enough to dent purchasing power.

When rates sit at that level, buyers tend to do two things:

They get pickier.

They get price-sensitive.

Meanwhile, many homeowners are still anchored to the emotional idea that “prices always go up,” or “my neighbor got X last year.”

But the data is a humbling reality check: housing markets can flatten out, and even small percentage swings can be enormous in dollar terms—especially in California, where statewide medians are still in the $800Ks range. If you’re in the Sonoma County sweet spot (often around $900K–$1.5M depending on the area), a tiny market shift can equal a major paycheck.

On a $1,000,000 home, a 10% swing = $100,000.

On a $1,200,000 home, an 8.3% swing = $100,000.

Most homeowners don’t consciously decide to lose 10%. They drift into it:

Start too high → sit → reductions → stale listing → bigger reductions

Wait too long → more inventory → buyers negotiate harder → lower net proceeds

This is the cousin of the “wait until rates drop” strategy, and it can be just as expensive.

Here’s what happens:

You list high to “leave room.”

Buyers ignore it and move on.

After 2–4 weeks, the listing is psychologically “old” to the market.

You reduce.

Now it’s not “exciting”; it’s “what’s wrong with it?”

Offers come in—if any—at an even deeper discount.

The price reduction isn’t the problem. The timing is.

In a market with rates hovering around the mid-6s, you can’t rely on sheer demand to rescue a listing strategy. Buyers are more cautious, and the best ones are trained to spot overpriced listings from a mile away.

A lot of homeowners forget that “selling for less” isn’t just about the gross price—it’s about the net.

Here’s how the mistake compounds:

If it takes you 3–6 extra months to get the home sold, you’ve paid:

mortgage interest

taxes

insurance

utilities

maintenance

possible HOA

and the “invisible cost” of your time/stress

Even $3,000–$5,000/month for a few months is real money. But the bigger cost is the negotiation power you lose when your listing is old.

Markets don’t have to “crash” to penalize you. A market can go sideways while you go down.

Think of it like this:

A home enters the market competitively and sells.

Your home sits.

A new set of comps gets established.

Your price now looks even less justified.

You reduce again… and now you’re negotiating from a position of weakness.

Fresh listings create urgency. Stale listings create “let’s wait and see.”

In 2026, with mixed macro signals and buyers watching affordability, that psychological shift matters even more.

If you want one action item, make it this:

Price for the market you’re in, not the market you wish you were in.

That doesn’t mean “price low.”

It means:

study the most recent neighborhood closings (not headlines)

respect the competition currently on the market

price in a way that generates strong early activity (days 1–14 matter)

pair price with presentation (staging/cleaning/minor fixes can be ROI monsters)

use a data-backed strategy—not hope

In fact, even broader forecasts for 2026 show modest expectations. A Reuters poll recently found analysts expecting U.S. home prices to rise only around 1.8% in 2026—not exactly “rocket fuel.” In that kind of environment, the edge goes to sellers who are strategic, not nostalgic.

It depends.

But here’s the honest bottom line:

If you’re planning to sell anyway, the most expensive move is usually procrastination without a strategy. “We’ll just wait” is not a strategy.

A strategy is:

when you’ll list

what you’ll do to prep

how you’ll outcompete similar listings

how you’ll control narrative and urgency

how you’ll defend your net proceeds in negotiations

In other words, the difference between an $850K sale and a $950K sale is rarely just luck. It’s preparation and positioning.

If you want, I can run a quick “$100K risk check” on your property:

what it would likely sell for in the next 30–90 days

what you’d net after selling costs

how to avoid discounting yourself through timing/pricing

and what small improvements could boost your price-per-foot

No obligation. No pressure. Just clarity—so you don’t wander into the $100K mistake.

If you tell me your neighborhood or a rough price range, I’ll tailor this into a Sonoma County–specific version with a stronger hook and the exact comps/strategies your area responds to best.

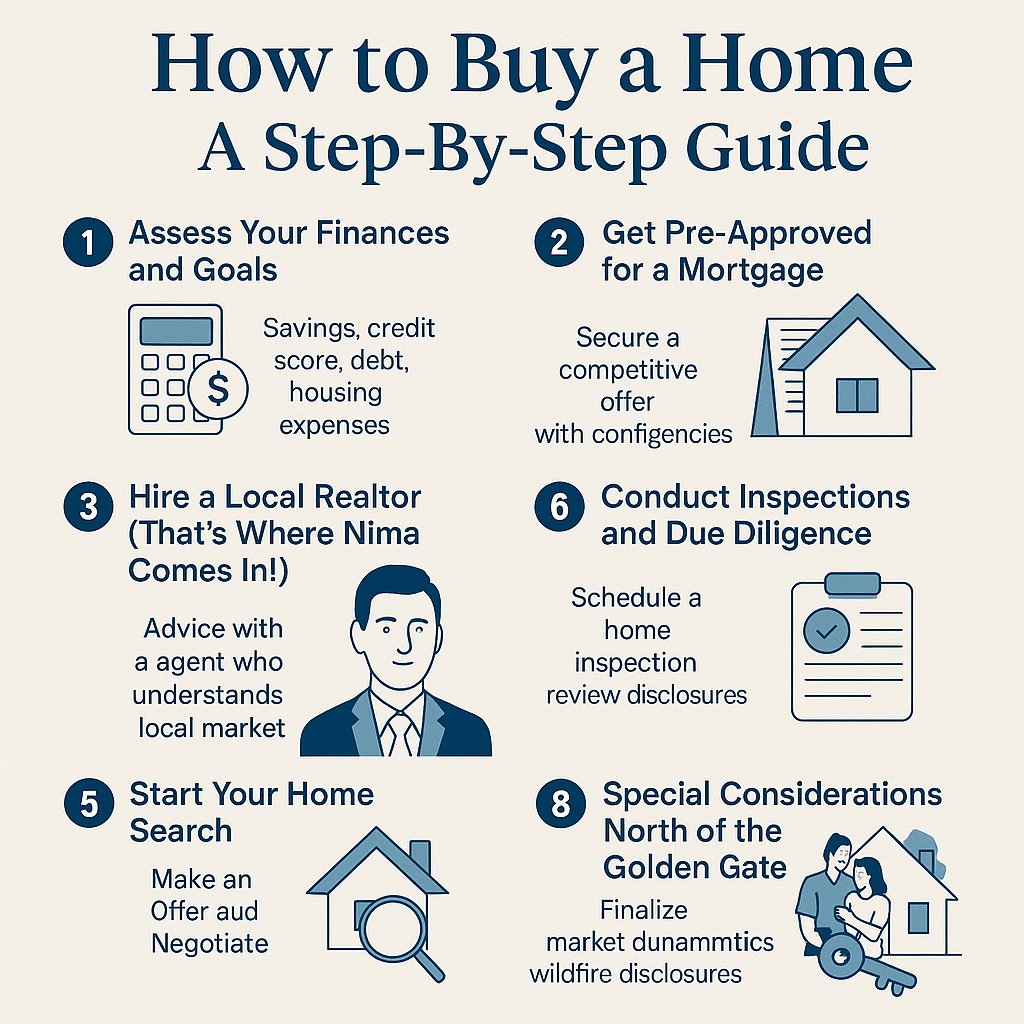

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!