The Real Cost of Buying a Home in 2026 (It’s More Than Just the Price)

Nima Kazeroonian January 27, 2026

Nima Kazeroonian January 27, 2026

Buying a home in 2026 isn’t just about finding the right house at the right price. For many buyers—especially first-time and move-up buyers—the biggest surprise isn’t the mortgage payment. It’s everything around the purchase that adds up quickly.

I see this all the time with buyers in Sonoma County. The purchase price gets all the attention, but the real cost of buying a home is made up of several moving parts, and understanding them upfront can save you stress, money, and regret later.

This guide breaks down what buyers should realistically expect to pay in 2026—in plain English, without the fluff.

Let’s start with the obvious. The purchase price is the number you see online and the number your mortgage is based on. In 2026, prices across Sonoma County remain highly neighborhood-specific. Two homes just miles apart—or even on the same street—can still command very different prices based on condition, layout, lot size, and buyer demand.

But here’s the key point: the purchase price is only the starting line, not the finish.

One of the biggest myths in home buying is that you need 20% down. In reality, many 2026 buyers are using:

3%–5% down conventional loans

3.5% down FHA loans

0%–10% down VA loans (for eligible buyers)

That said, your down payment directly impacts:

Your monthly payment

Whether you pay mortgage insurance

How competitive your offer looks to a seller

In competitive Sonoma County markets, buyers who can put more down often gain leverage—but that doesn’t mean it’s always the smartest financial move. Strategy matters more than a blanket rule.

Closing costs are where many buyers get caught off guard.

In 2026, buyers should generally budget 2%–3% of the purchase price for closing costs, which may include:

Loan origination fees

Appraisal fee

Credit report

Escrow fees

Title insurance

Recording fees

Prepaid interest

Initial property tax and insurance escrows

On a $750,000 home, that can easily mean $15,000–$22,500 due at closing—on top of your down payment.

Some buyers negotiate seller credits to offset these costs, but that depends heavily on market conditions, pricing strategy, and how clean your offer is.

In 2026, buyers are far more rate-aware than they were a few years ago—and for good reason.

Interest rate affects your monthly payment

APR (Annual Percentage Rate) reflects the true cost of the loan, including fees

Two loans can advertise the same rate but have very different APRs depending on points, lender fees, and structure. This is why comparing lenders purely on rate can be misleading.

Smart buyers compare total monthly cost and long-term impact, not just the headline number.

Home inspections are optional—but skipping them can be very expensive.

In Sonoma County, buyers often pay:

$500–$900 for a general home inspection

Additional fees for roof, pest, sewer lateral, or chimney inspections

Even when buying a newer or well-maintained home, inspections give you clarity. The goal isn’t to find a “perfect” house—it’s to understand what you’re buying and plan accordingly.

When demand outpaces inventory, appraisals don’t always keep up with contract prices.

If a home appraises for less than your agreed price, buyers may need to:

Renegotiate with the seller

Increase their down payment

Walk away (depending on contingencies)

This is where having financial flexibility—and a smart offer strategy—matters more than ever.

California property taxes generally run around 1.1%–1.25% of assessed value, depending on location and local assessments.

For buyers moving into higher-priced homes, this can be a meaningful jump from previous housing costs. Property taxes are typically paid monthly through your mortgage escrow, but they’re still part of your real cost of ownership.

Insurance has become a bigger conversation in 2026, especially in parts of Northern California.

Buyers should budget for:

Standard homeowners insurance

Possible FAIR Plan coverage

Higher premiums in certain areas

Insurance costs vary widely by property location, construction type, and coverage needs—and they should be reviewed early, not at the last minute.

Even “move-in ready” homes usually come with expenses buyers don’t expect:

New locks

Minor repairs

Interior paint

Window coverings

Furniture adjustments

Landscaping touch-ups

These aren’t deal-breakers, but they should be part of your upfront budget planning.

The true cost of buying a home in 2026 isn’t meant to scare buyers—it’s meant to prepare them.

Buyers who understand the full picture:

Make stronger offers

Feel more confident

Avoid last-minute stress

Enjoy their home more after closing

That’s the difference between buying reactively and buying smart.

Every buyer’s situation is different. Your income, savings, loan type, timeline, and goals all shape what buying should look like for you.

If you’re thinking about buying in Santa Rosa, elsewhere in Sonoma County, or even just starting to explore your options, I’m happy to walk through the numbers with you—no pressure, no assumptions.

Sometimes the most valuable thing isn’t a house—it’s clarity.

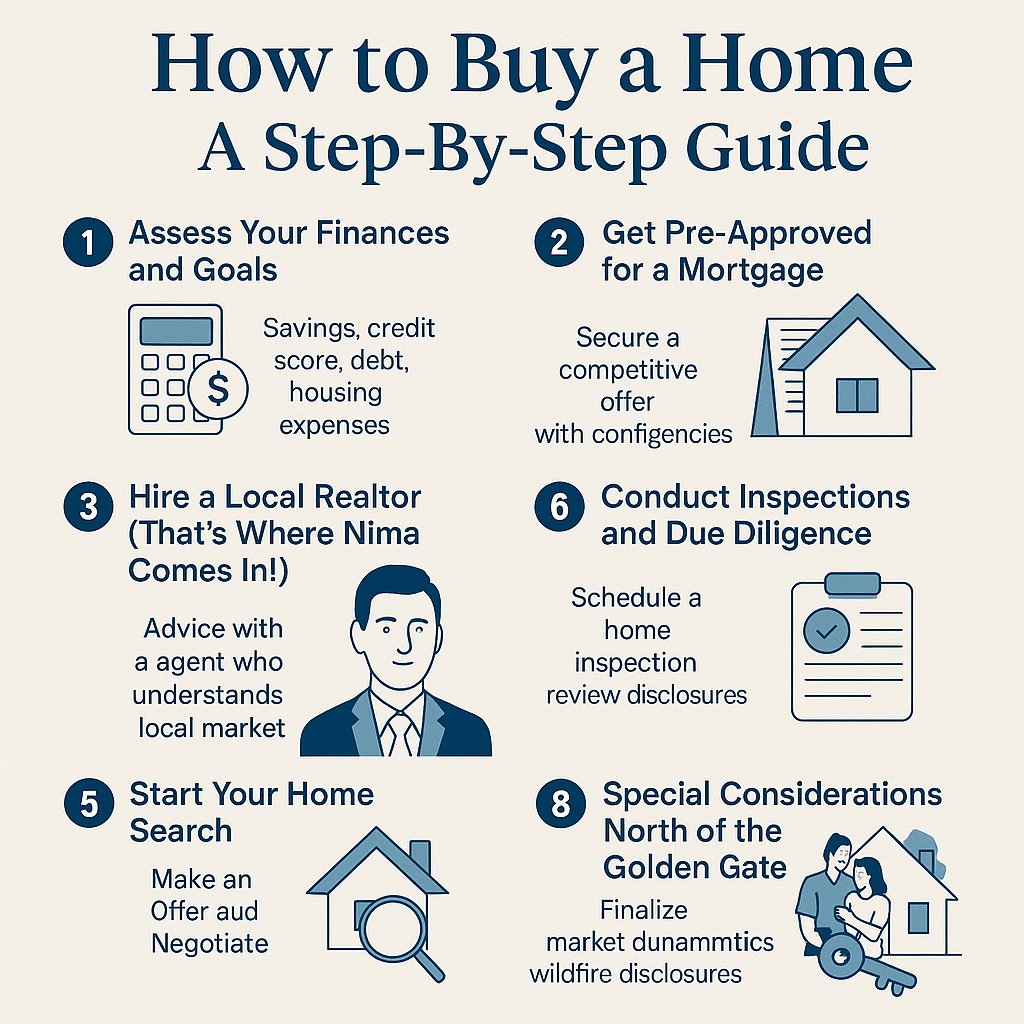

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!