The Truth About Rising Home Insurance Costs in Sonoma County — What’s Really Happening & How Homeowners Can Lower Their Premiums

Nima Kazeroonian November 26, 2025

Nima Kazeroonian November 26, 2025

If you own a home in Sonoma County, you’ve probably felt the sting of rising insurance premiums. Rates have climbed sharply over the last five years—especially in areas labeled “high fire-risk zones.” But the story behind these increases is more complex than simple risk scoring. State regulations, carrier exits, wildfire modeling, and new mitigation rules all play a part.

Here’s what homeowners need to know right now—and the steps that can actually reduce insurance costs in 2025–2026.

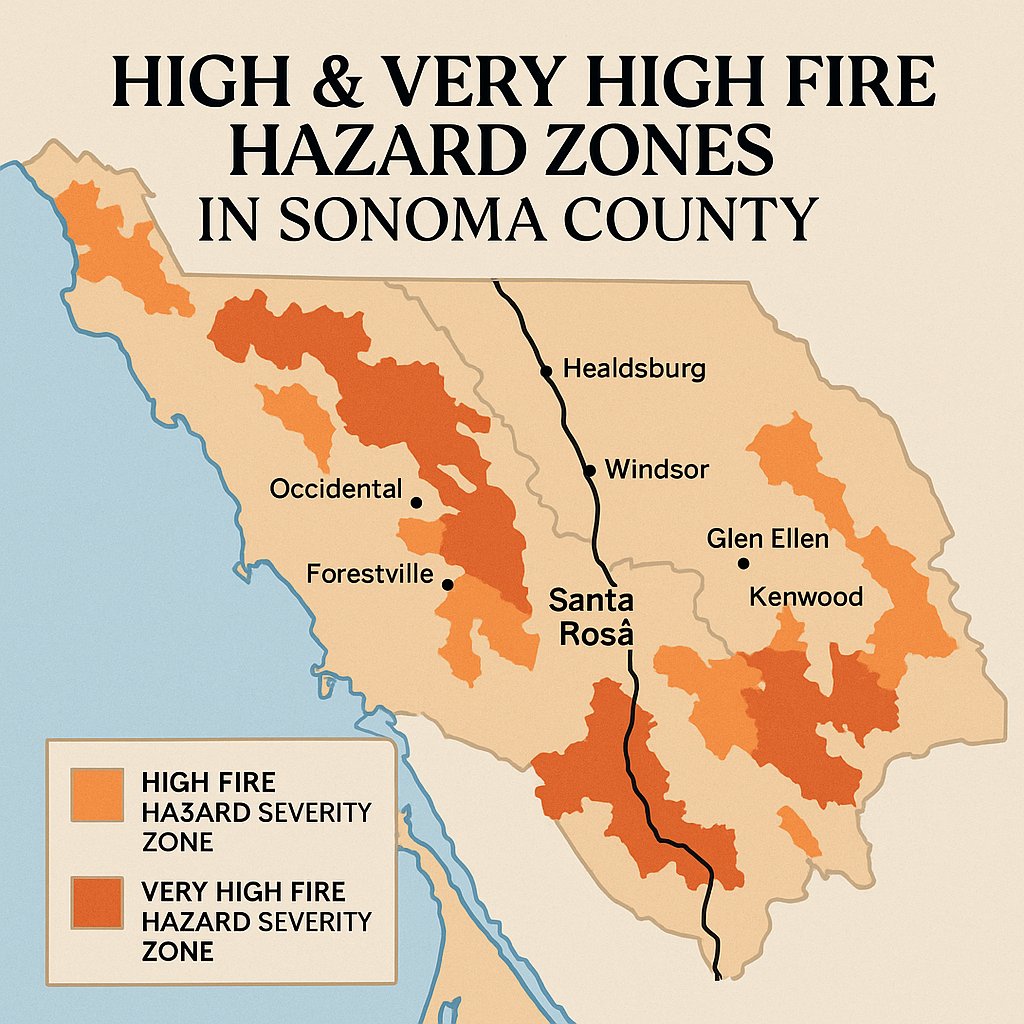

Large portions of Sonoma County fall into CalFire’s “High” or “Very High” Fire Hazard Severity Zones—especially in:

Santa Rosa (Fountaingrove, Bennett Valley, Montecito Heights)

Healdsburg

Windsor foothills

Glen Ellen, Kenwood

West County (Occidental, Forestville, Guerneville)

When a home is inside these zones, insurers apply higher premiums due to increased wildfire exposure.

Over the last few years, several carriers paused new policies or tightened underwriting. Why?

Higher wildfire losses

Reinsurance costs skyrocketing

State regulations limiting rate increases

Carriers shifting away from rural/wildland-urban interface areas

Some insurers are gradually returning, but under stricter conditions—and often tied to mitigation improvements.

Insurers now use more detailed wildfire-risk models that evaluate:

Slope and topography

Distance to open wildland

Wind patterns

Evacuation access

Neighborhood vegetation density

Two homes on the same street can get completely different quotes based on these factors.

This is one of the top factors insurers look at. Key actions include:

Removing brush and ladder fuels

Trimming tree limbs 6–10 ft off the ground

Clearing roofs and gutters

Replacing mulch near structures with gravel

Some carriers reduce premiums after you provide before/after photos.

Upgrades that make a major difference:

Class A fire-rated roof

Stucco, cement board, or ignition-resistant siding

Ember-resistant vents

Dual-pane tempered windows

5-feet non-combustible zone around the home

These improvements can push your property into a better risk tier.

Insurers want to see:

Hydrants within 1,000 feet

Clear driveway access

Room for fire truck turnaround

In rural areas, adding a permitted water storage tank can help with eligibility.

If your neighborhood participates in Firewise, some insurers offer discounts up to 10%.

Slowly—yes.

As California’s new insurance regulations roll out, several carriers have signaled they will re-enter the market. But expect:

Tight underwriting

More documentation

Required mitigation for older homes

Premiums won’t drop overnight, but competition will gradually improve.

Work with brokers who can access:

Surplus lines carriers

Regional insurers

High-risk programs

Some can beat FAIR Plan pricing depending on your zip code.

Bundling home and auto can save 10–20%.

Increasing from $1,000 to $2,500 can meaningfully reduce premiums.

Many carriers now allow inspections that confirm:

Defensible space

Hardened features

Ember-resistant venting

Roofing materials

Passing can drop your premium immediately.

Most homeowners overpay simply because they stay with the same policy for too long. Rates shift constantly—especially in Sonoma County.

Insurance rates are high—and fire-zone mapping is a big driver—but homeowners have more control than they think. Strategic mitigation, home-hardening, bundling, and yearly reviews can lead to real savings. And as insurers slowly return to the California market, options should expand in 2025–2026.

If you want help understanding how insurance changes impact your property’s value, marketability, or selling strategy, I’m always here to walk you through it.

Along with this checklist, seeking guidance from a professional is always a good idea!

Gov't Shutdown

Less competition, motivated participants, and market insights for the season

When to hire Nima, secure pre-approval, and navigate the North Bay market

Exploring the pros and cons of homeownership versus renting across different time horizons

Whether you're buying, selling, or exploring options, Nima is dedicated to making the process smooth, informed, and rewarding. Reach out today for a personalized consultation and let’s make your real estate goals a reality!